Know Your Customer (KYC) Compliance

KYC

Know Your Customer (KYC) is the process of validating your clients' identities before or during the time they begin doing business with you. KYC also refers to the regulated bank customer identification verification methods used to assess and manage client risk. The KYC procedure is also a legal requirement meant to combat anti-money laundering (AML).

Know Your Customer integrates disparate systems and time-consuming manual procedures with a single integrated KYC and AML solution, resulting in enhanced compliance and superior client onboarding. Also, the procedure entails confirming that the customer is who he claims to be and granting him access to the services or products he needs. This verification is done out using several approaches, not all of which meet with legal standards.

KYC COMPLIANCE

KYC compliance has a significant influence on how financial services organizations enable users to register accounts and conduct financial transactions on their preferred device. Customers want to bank online, but banks must comply with AML and KYC regulations while simultaneously combating fraud and financial crimes and minimising high-risk transactions.

According to regulatory rules, obligated entities implement customer identification systems and verify their consumers on a regular basis. Furthermore, it assists organizations in avoiding fines, combating fraud, and mitigating financial crimes (money laundering, terrorist financing).

THE KYC - PROCESS

Financial institutions begin the KYC process by requesting basic information from clients about their company operations and persons. It contains information such as the names of the directors, business addresses, national insurance or social security numbers, company numbers, and so on. This information is complemented by openly accessible information about the company, such as names and locations, registration numbers, stock market listings, and annual reports.

To combat identity theft, money laundering, and financial crime, current KYC procedures take a risk-based approach:

- Theft Identification: KYC assists financial companies in establishing legal verification of a customer's identity. This can help to avoid phoney accounts and identity frauds caused by counterfeit or stolen identification papers.

- Money laundering: Drugs, human trafficking, smuggling, racketeering, and other illegal activities utilise fake accounts in banks to hold funds for narcotics, human trafficking, smuggling, racketeering, and other activities. These illegal sectors try to evade suspicion by dispersing the money across many accounts.

- Financial Fraud: KYC is intended to prevent fraudulent financial activity such as applying for a loan with a fake or stolen ID and then receiving funds with a fraudulent account.

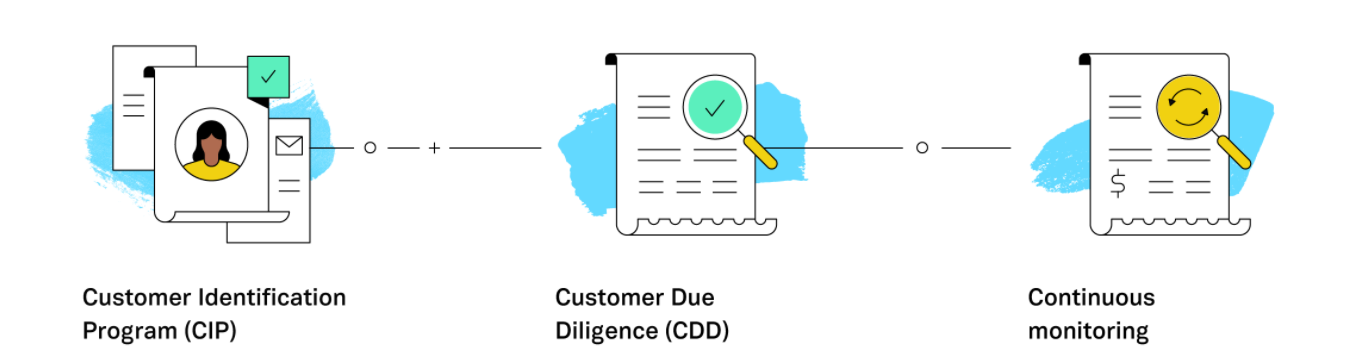

THE KYC – COMPONENTS

The three components of KYC are as follows:

- Customer Identification Program (CIP): The customer is who they claim to be.

- Customer Due Diligence (CDD): Assess the customer's degree of risk, including an examination of a company's beneficial owners.

- Continuous monitoring: Ongoing monitoring of customer transaction trends and reporting of questionable behaviour.

Important KYC Laws

Most of the time, KYC requirements are part of AML regimes and are inspired by FATF guidelines. The following is a list of various KYC legislation that have been established across the world.

- Banking Secrecy Act (BSA) of the United States mandates reporting institutions (mainly banks) to take the appropriate steps for client verification and to report suspicious activity to FinCEN. According to the terms of the US Patriot Act, banks are obligated to implement customer identification procedures.

- Anti-money laundering Act (AMLA) of France defines the legislation governing consumer identification verification for financial institutions.

- The Money Laundering Act – 2017 (MLA): The Customer Verification Regulations for Reporting Entities are defined by the United Kingdom.

KYC Compliance in a Digital World

Manual KYC is an insufficient answer to the threat posed by money laundering typologies in data-driven digital asset ecosystems. Firms can manage digital AML compliance issues and improve client experiences by automating the KYC process. The following are some of the specific benefits of KYC automation:

-

Speed and productivity:

Automated KYC allow businesses to keep up with the speed of digital asset transactions by executing customer due diligence, transaction monitoring, and screening procedures swiftly and efficiently. Before criminals can convert unlawful cash or move them into the normal financial system, firms will be able to establish client identities, categorise them based on risk profile, and monitor their transactional history for suspicious activities.

-

Precision and Capacity:

Automation helps organisations to use advanced search technologies that give more accurate results while reducing expensive noise and false positives, rather than manually combing through sanctions lists and watch lists on an individual basis. Dedicated search engines and risk databases updated with the latest sanctions and blacklist information are among the upgraded KYC capabilities, allowing companies to detect changes in a customer's risk profile promptly.

-

Ongoing compliance:

With the cryptocurrency ecosystem quickly developing and regulatory fines growing, automation helps businesses to manage their compliance performance on a continuous basis. Smart technology automation enables 'horizon scanning,' allowing businesses to anticipate potential changes in money laundering type as well as new legal requirements imposed by international bodies such as the FATF's Travel Rule and the EU's Fifth and Sixth Anti-Money Laundering Directives.